Federal Reserve policymakers are about to take their first break from an interest-rate hiking campaign that started 15 months ago, even as they confront a resilient US economy and persistent inflation.

The Federal Open Market Committee on Wednesday is expected to maintain its benchmark lending rate at the 5%-5.25% range, marking the first skip after 10 consecutive increases going back to March of last year. While officials’ efforts have helped to reduce price pressures in the US economy, inflation remains well above their goal.

Investors’ focus will be on the Fed’s quarterly dot plot in its Summary of Economic Projections, which is expected to show the policy benchmark rate at 5.1% at the end of 2023.

By contrast, markets are pricing in the possibility of a quarter-point hike in July followed by a similar-sized cut by December, and some Fed policymakers have emphasized that a pause in the hiking cycle shouldn’t be seen as the final increase.

Fed Chair Jerome Powell, who’ll hold a press conference after the meeting, has suggested he favors a break from hiking to assess the impact both of past moves and of recent banking failures on credit conditions and the economy. His commentary will be scrutinized for hints of the committee’s plans at its following meeting next month.

What Bloomberg Economics Says:

“Discord on the FOMC is mounting. Those who prefer to skip a hike in June want to wait and see — given the long and variable lags of monetary policy — how 500 basis points of rate hikes to date are cooling the economy. More hawkish members are convinced rates aren’t yet restrictive enough, and the Fed shouldn’t risk falling behind the curve. We see a ‘hawkish skip’ as a way to maintain unanimity on the committee.”

—Anna Wong, Stuart Paul, Eliza Winger and Jonathan Church, economists. For full analysis, click here

Fed officials will have new consumer price index data in hand when they start their monetary policy deliberations on Tuesday. While central bankers target a separate inflation measure for their 2% goal, the closely watched CPI report is expected to show still-stout underlying price pressures.

The core gauge, which excludes volatile food and energy prices, is seen rising 0.4% from a month earlier. That would mark the sixth-straight month that core inflation has increased by that much or more, and helps to explain why interest rates may stay elevated for longer.

Monthly advances of that magnitude have made it difficult for underlying inflation to cool quickly. On a year-over-year basis, the core CPI is expected to rise 5.2%, the slowest pace since November 2021. The overall CPI is projected to recede to 4.1%. While still uncomfortably high, gradually moderating inflation provides some space for the central bank to pause.

A report on Wednesday is projected to show further disinflation at the producer level, with a core gauge seen rising at the slowest annual pace in more than two years as goods costs continue to settle back.

May retail sales round out top US economic data this coming week. The value of purchases was probably little changed during the month, consistent with softer consumer demand for merchandise.

Further north, Canada’s tight housing supply will be a focus after a revitalized real estate market helped prompt a resumption of rate increases. Data on Thursday will show whether housing starts kept falling in May, eroding the potential supply of homes amid record immigration, and if existing home sales kept rising too.

Elsewhere in the world, the European Central Bank is likely to keep raising rates, the Bank of Japan may remain on hold, and Chinese monetary officials could avoid adding stimulus for now.

Click here for what happened last week and below is our wrap of what’s coming up in the global economy.

Europe, Middle East, Africa

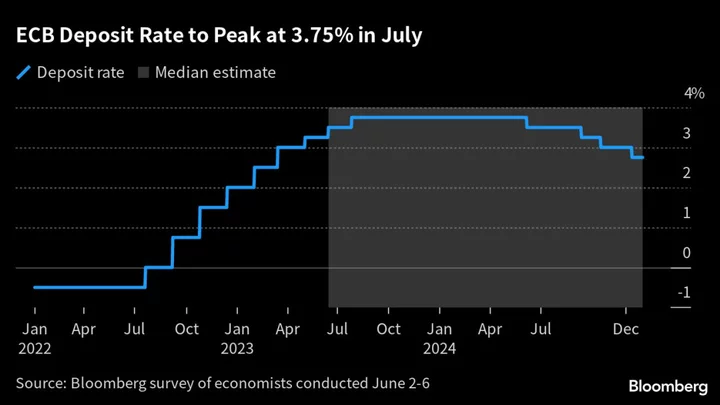

The day after the Fed decision, ECB officials are almost certain to diverge from their US counterparts and press on with rate increases. Economists expect a second consecutive quarter-point move. With another hike also widely touted for July, the focus is likely to fall on the details of new quarterly forecasts and on any hints about prospects for yet another move in September.

Further to that, a final take on euro-zone inflation in May will be published on Friday, along with the ECB’s survey of professional forecasts, illustrating the collective view of the economics community on the central bank’s outlook.

In the Nordic region, Danish inflation will be released on Monday, and later in the week, monetary officials there may follow the ECB’s rate decision with a hike of their own, as they typically do.

Meanwhile, monthly growth data in Norway and inflation and consumer expectations data in Sweden will be informative for central banks in those countries, which are still in tightening mode.

Further east, the Ukrainian central bank will announce its key rate decision at a time its war-torn economy appears to be improving faster than previously estimated.

Central banks across Africa will make decisions in the coming week as well:

- On Tuesday, the Bank of Uganda’s monetary policy committee will likely hold its key rate for a third successive meeting after inflation slowed sharply in May to 6.2%.

- The following day, Namibian officials will probably increase borrowing costs to safeguard their currency peg with the rand after neighboring South Africa raised rates by 50 basis points.

- Central banks in Botswana and Mauritius are both expected to hold rates steady on Thursday, with inflation projected to continue slowing toward their targets.

Thursday’s also a big day for fiscal announcements. Kenya, Tanzania, Uganda, Rwanda and Burundi will unveil budgets expected to increase spending to boost recoveries from shocks such as droughts, the pandemic and Russia’s war on Ukraine.

Saudi Arabian data on Thursday is likely to show inflation steadied in May, and will probably be close to the 2.7% seen in April. The kingdom’s economy has slowed in the past three quarters, in large part because of global weakness causing a drop in oil prices.

The same day, investors will be watching whether Israeli inflation accelerated in May as the shekel weakened. The currency fell 2.7% against the dollar last month on renewed concerns over Prime Minister Benjamin Netanyahu’s plan to overhaul the judiciary.

- For more, read Bloomberg Economics’ full Week Ahead for EMEA

Asia

Key Chinese economic indicators set for release on Thursday will likely show a slowdown in consumer and business activity in May as the post-pandemic boost fades.

The People’s Bank of China will have an opportunity to add more monetary stimulus, although the majority of economists surveyed by Bloomberg predict no change to rates just yet.

Hong Kong and Taiwan will also announce rate decisions on Thursday.

The Bank of Japan has its second policy meeting under Governor Kazuo Ueda at the end of the week. Most economists expect no change this time as speculation rumbles on that Prime Minister Fumio Kishida is mulling an early election.

Trade figures from Japan, India, and Indonesia on Thursday are set to show the latest state of global demand, while New Zealand also reports on its first quarter growth that day.

- For more, read Bloomberg Economics’ full Week Ahead for Asia

Latin America

Brazil’s retail sales data for April won’t likely maintain the pace seen in the strong close to the first quarter, giving President Luiz Inacio Lula da Silva more reason to hector the central bank in pursuit of lower rates.

Similarly, Brazilian GDP-proxy data for April will likely falter as Latin America’s biggest economy down-shifts from much-stronger-than-expected first-quarter output readings.

Central banks in Brazil, Colombia and Chile publish surveys of economists’ expectations, with Banco Central de Chile also posting a separate survey of traders.

Colombia posts April manufacturing, industrial output and retail sales results, which turned negative in March as the the highest borrowing costs since 1999 weighed on consumers and companies and undercut confidence.

Peru’s monthly GDP-proxy reading for April is likely to build on March’s rebound with mining operations normalizing after labor disruptions and civil unrest in the country’s south.

Argentina’s May inflation report should show a 16th straight rise in consumer prices pushing the annual rate over 116%, against the current 108.8%.

Low international reserves, an overvalued peso and presidential elections in October suggest the government lacks the tools and likely won’t have the appetite to do much about inflation before year-end.

- For more, read Bloomberg Economics’ full Week Ahead for Latin America

--With assistance from Robert Jameson, Monique Vanek, Michael Winfrey and Laura Dhillon Kane.

Author: Steve Matthews, Vince Golle and Craig Stirling