The Federal Deposit Insurance Corp. on Wednesday will publish a comprehensive report on the health of the banking system in the period when Silicon Valley Bank and Signature Bank failed.

The FDIC’s Quarterly Banking Profile, which will cover the first three months of 2023, is by definition backward-looking. However, the edition spans a particularly tumultuous period during which three US banks buckled, and analysts speculated about the viability other small and midsize lenders.

In one closely watched metric, the regulator will release the aggregate number and assets of lenders on its confidential “Problem Bank List.” In its previous edition, which covered the final three months of 2022, the FDIC said that the number of firms on the list had fallen to 39. The report will also provide information on the government’s bedrock deposit insurance fund, which was drained by making clients at the failed lenders whole.

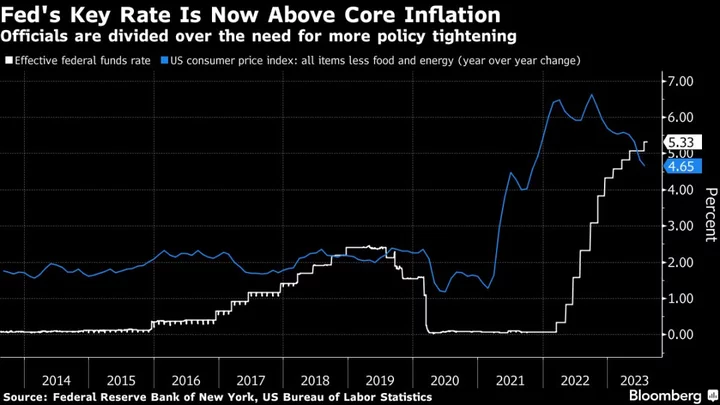

In releasing its previous report, FDIC Chairman Martin Gruenberg said the agency found key banking industry metrics remained favorable, adding that the sector continued to face significant downside risks from inflation, rising market interest rates, and geopolitical uncertainty. Analysts will be closely watching his remarks on Wednesday for new assessments.

Silvergate Capital Corp. kicked off a wild three months in the banking sector on March 8 when it announced plans to wind down operations and liquidate its bank. Just two days later, Silicon Valley Bank collapsed into what was then the second-biggest failure in US history. Then on March 12, financial regulators closed Signature Bank and declared it to have failed.

Since March, stresses have continued. In the latest shoe to drop, First Republic was seized by the FDIC on May 1 after a flood of customer withdrawals and declining asset prices. The regulator struck an agreement for JPMorgan Chase & Co. to take over the bank’s $173 billion of loans and $30 billion of securities, as well as $92 billion in deposits, after talks to rescue the lender dragged on for weeks.