BlackRock Inc. and Aviva Investors are among fund managers looking to benefit from a further slowdown in UK inflation after loading up on government bonds.

They’ve been piling into gilts to grab yields at the highest in more than 15 years, in a bet that the Bank of England will pivot to cutting interest rates. Two key data releases this week may determine whether that starts to pay off — a jobs report on Tuesday and then inflation figures a day later.

It’s a brave wager given the pain bonds have caused money managers in 2023. Bloomberg’s gilt index shows investors have lost more than 4% this year, while a fresh spike in oil prices risks more inflationary pain. That’s got money markets expecting the BOE will have to hold off on any rate cuts for nearly a year.

“Our view is that long-term UK policy rates will be lower than the market is pricing,” said Vivek Paul, UK chief investment strategist at the BlackRock Investment Institute. “We recently went overweight UK gilts because of their attractive yields.”

Tuesday’s jobs report will give bondholders insight into whether wage pressures are moderating, while inflation figures for September are seen slipping to the lowest in 20 months. Both will provide valuable information for the BOE as it prepares for a policy decision on Nov. 2.

Policymakers are keeping a particularly close eye on median pay for signs of a wage-price spiral. Catherine Mann, the most hawkish member of the BOE’s Monetary Policy Committee, said this month that policy needed to remain “aggressive” for precisely that reason.

“The key figure will — once again — be private sector regular pay growth,” said Bruna Skarica, UK economist at Morgan Stanley. She expects the three-month rate to edge down to 7.9% on a year earlier, from 8.1% last month.

If wage growth does indeed temper, and figures due on Oct. 24 show unemployment rising, the BOE “shouldn’t hesitate” to keep rates at 5.25% next month, said Sam Tombs, chief UK economist at Pantheon Macroeconomics.

Read more: UK Interest Rates ‘Finely Balanced’ as BOE Inflation Fight Bites

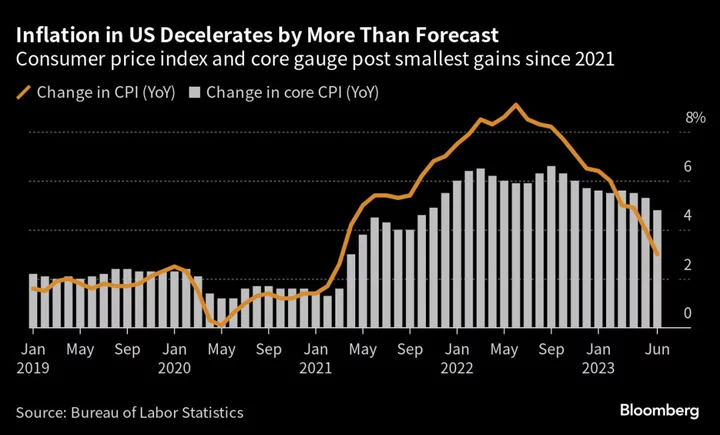

Inflation on Wednesday also looks tricky to call. Falling food and core goods prices are expected to bring the headline rate down a touch to 6.6%, though rising fuel costs will counter some of this. Skarica said the “key unknown” is services inflation, while Ruth Gregory, deputy chief UK economist at Capital Economics, said the “upside risks to oil and gas prices” from the Israel-Hamas conflict will add to BOE concerns about whether it has done enough.

Data on UK economic activity so far is painting a picture of a country struggling to generate any momentum in growth. This will surely be weighing on policymakers’ minds as they try to toe the line between getting inflation down and avoiding an unnecessary recession.

That’s leading money-market traders to favor another rate pause by the BOE next month, with only a 30% chance seen for another hike. Even though the most aggressive policy tightening in decades may be nearly over, markets don’t expect cuts to start until September 2024.

Bets on Cuts

Plenty of big funds are betting the BOE will have to move faster. London-based Aviva Investors, which manages more than £226 billion ($275 billion), has been buying UK debt on the “reasonable probability” the BOE will end up cutting rates by more than 100 basis points next year. That’s twice as much as money markets expect.

“Declines in UK house prices, gradual signs of moving towards higher unemployment in the UK — those are exactly what you would expect to see to call a peak in rates,” said Sunil Krishnan, head of multi-asset funds at Aviva. “Right now there is a non-trivial risk of the UK having to move into a meaningful cutting cycle and I don’t think that’s reflected in the prices.”

Foreign buyers are also being attracted to UK debt. They’ve now bought more than £57 billion in the five months through to August, the second most ever in that time span, according to data published by the BOE. A weak pound, near $1.20, is helping.

While any signal from the economic data that policy easing may come sooner would launch a bond rally, there’s been plenty of false starts before. US inflation data for September came in higher than expected last week, driving a fresh selloff in Treasuries and gilts.

Read more: Time Is Running Out for the ‘Year of the Bond’ as Losses Mount

Even so, UK yields have still fallen in the past week, with the gilt market now being supported by haven demand from concerns the Israel-Hamas conflict could widen in the Middle East. That’s likely to help cap any selloffs in the short term. Long-maturity gilts have been among the biggest beneficiaries of the rush to safety.

“We think that the worst for gilts is over,” said Evelyne Gomez-Liechti, a multi-asset strategist at Mizuho International Plc in London.

--With assistance from Anchalee Worrachate and Sujata Rao.