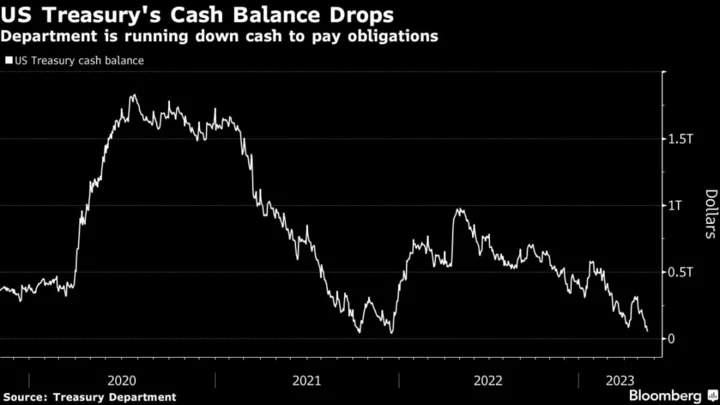

Investment bank clients are peppering Wall Street with questions about what happens if the US Treasury in coming weeks runs out of cash and does the unthinkable — failing to make payments due on Treasury securities, the bedrock of the global financial system.

With the clock ticking to June 1, the date by when Treasury Secretary Janet Yellen has advised her department may run out of sufficient cash, as of Monday there was still no deal announced between President Joe Biden and Speaker Kevin McCarthy on raising the federal debt ceiling.

Market participants have long assumed that, if the Treasury ran out of sufficient cash during a partisan debt-limit showdown, it would prioritize interest and principal payments on publicly held Treasuries. That $24 trillion market serves as a global benchmark for borrowing costs, serves as vital collateral for funding in money markets and forms a core part of asset holdings the world over.

The assumption has never been tested, however, and Treasury officials have long cast doubt in public about whether prioritization is practicable. So given the intensity of the current showdown, market participants are gaming out scenarios.

One school of thought is that the impact might not be so damaging. After all, since the 2011 debt-limit crisis, market participants have worked out a process for dealing with the Treasury announcing that it couldn’t make an interest or principal payment.

Read More: Debt-Ceiling Anxiety Tracker: Growing Fear Premium in Bills

But JPMorgan Chase & Co. Chief Executive Officer Jamie Dimon warned earlier this month that even going to the brink is dangerous, with unpredictable consequences.

“The closer you get to it, you will have panic,” he said in a May 11 interview with Bloomberg Television. “The other thing about markets is that, always remember, panic is the one thing that scares people — they take irrational decisions.”

And even a key group that helped to compile the emergency procedures, the Federal Reserve Bank of New York-sponsored Treasury Market Practices Group, has issued its own caution.

“While the practices contemplated in this document might, at the margin, reduce some of the negative consequences of an untimely payment on Treasury debt for Treasury market functioning, the TMPG believes the consequences of delaying payments would nonetheless be severe,” it said in its December 2021 gameplan.

Broader disruption in financial markets would quickly put focus on the Fed, which during the 2011 debt-limit showdown compiled a backstop menu of options to avert systemic collapse. When reviewing those in 2013, then-board member Jerome Powell referred to two of them as “loathsome” — while stopping short of saying that he’d reject them.

Those two involved the Fed buying up defaulted Treasuries, or swapping them for non-defaulted securities on its balance sheet.

Powell, now the Fed’s chair, has repeatedly delivered the message in recent months that “no one should assume that the Fed can protect the economy” if Congress doesn’t address the debt limit.

Here are some of the scenarios that could unfold.

Fed’s Options

The US central bank is charged with maintaining financial stability, and in the event of major disruptions, Fed watchers assume that much of the playbook devised under former Chair Ben Bernanke still holds.

In addition to injecting short-term liquidity into financial markets, the Fed could also abandon its current quantitative tightening program of running down its holdings of Treasuries, Robert Perli and Benson Durham at Piper Sandler & Co. wrote in January. Perli has since become the head of the New York Fed’s markets desk.

As far as the default process goes, the contingency plan compiled by market participants would have the Treasury inform, by 10 p.m., that it wouldn’t be making a payment due the next day. A security for which a principal payment was due would have its maturity extended by one day.

Downgrade Likely

That message would be communicated over Fedwire, a network established for distributing Treasury payments on debt securities.

A missed payment on Treasury debt would trigger a downgrade of the sovereign rating, William Foster, a senior credit officer at Moody’s Investors Service said in an interview. For Moody’s, that would mean taking the US down to AA1 from AAA.

“There could be a missed interest payment that would be delayed a few days,” Foster said. “But there would be no loss to investors, and that would be important,” he said, based on the assumption that a deal would quickly emerge in Washington to raise or suspend the debt ceiling.

Delayed payments on particular securities don’t trigger a broader state of default on all debt outstanding — something known as a cross-default provision.

‘Localized’ Impact

That’s why it’s possible that immediate impact could be somewhat limited.

“We are likely to see localized dislocations in the event of missed payment,” if that were to happen, JPMorgan rates strategists, co-led by Jay Barry, wrote Friday in a Q&A for clients on a technical default.

RBC Capital Markets strategists, also writing Friday, said they “doubt” a downgrade would trigger any forced reallocation by fund managers away from Treasuries.

At the same time, RBC’s Blake Gwinn and Izaac Brook cautioned that the “back-office issues” of delaying payments “could very easily bleed into the front-office, causing disruptions to liquidity and market functioning.”

‘Biggest Risk’

The TMPG noted that some market participants “might not be able to implement” the contingency plans, “and others could do so only with substantial manual intervention in their trading and settlement processes, which itself would pose significant operational risk.”

It’s a dynamic that Robert Toomey, a managing director at the Securities Industry and Financial Markets Association, the top US association for broker-dealers, investment banks and asset managers, pointed to earlier this year.

“In real-time what the impact would be in the market is very much an open question,” he said in an interview. “The biggest risk is that we don’t know what will happen to the pricing” and the desirability of purchasing Treasuries, he said.

That indeed was a key concern Powell had during the 2013 debt-limit showdown. In the event of investors shunning Treasuries, the government could find insufficient demand at an auction of debt — which would be devastating, because the Treasury relies on selling new debt to pay off maturing securities.

Failed Auction

“The real risk is of a failed auction — is the loss of market access at any price,” Powell said in 2013, according to a Fed transcript of policymakers’ discussions.

Yellen, who was vice chair during the Fed’s 2011 and 2013 discussions, in an NBC interview on Sunday declined to specify what will happen if the Treasury does end up running out of cash.

“There will be hard choices to make if the debt ceiling isn’t raised,” she said.