In the eyes of one investor at least, the Bank of England’s interest-rate hike on Thursday was the last of this cycle.

They placed a £625,000 ($795,000) bet via options that will deliver a payout eight times that amount if the central bank holds at 5.25% when it next meets in September, according to data compiled by Bloomberg. It would be the first pause after 14 consecutive hikes as policymakers scrambled to get soaring inflation under control.

To be sure, it’s an out-of-consensus view. The market is pricing a 90% chance of a quarter-point hike next month. Yet it speaks to how divided traders — who were already split ahead of Thursday’s move — remain about the bank’s intentions.

The BOE’s decision “had something for everyone,” said Andy Burgess, fixed income investment specialist at Insight Investment. “The bank remains data dependent, with inflation data released in the months ahead critical to how high rates ultimately go.”

The decision to forego a larger half-point increase was coupled with comments from policymakers about the toll rate hikes were already taking on the economy, fueling expectations the bank was nearing the end of its hiking cycle.

The Monetary Policy Committee also added guidance saying its stance would be “sufficiently restrictive for sufficiently long” to bring inflation back to the 2% target. Meanwhile, Governor Andrew Bailey cautioned that it was “far too soon to speculate on when we might see a cut.”

For now, money markets more broadly expect at least another 50 basis points of hikes, implying a peak rate of 5.75%. While that’s far less than what they were wagering on just a month ago, it’s more than the Federal Reserve and European Central Bank, both of which started raising rates later.

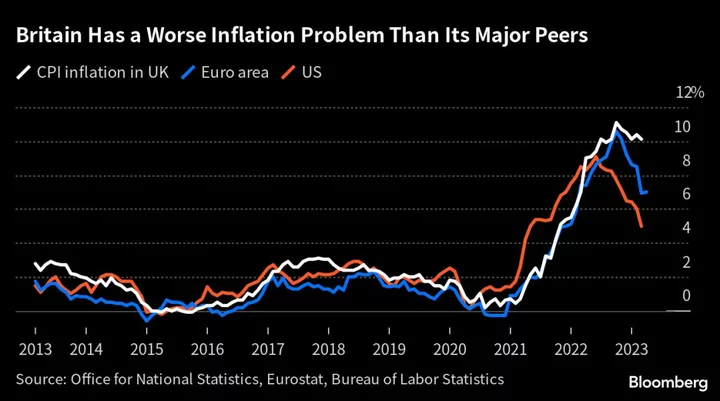

The challenge is that unlike the US and Europe, where inflation is showing solid signs of tempering, the outlook in the UK remains fraught, with price growth of 7.9% still four times the official target.

Economic Pain

At the same time, the BOE remains more constrained by the damage it risks inflicting on the nation’s fragile housing market. Signs of growing division among the nine-member Monetary Policy Committee are not helping either.

“The three-way vote split shows why it continues to be difficult to get a sense of the MPC’s reaction function,” said Samuel Zief, head of FX strategy at J.P. Morgan Private Bank.

For Zief, the decision to opt for a 25-basis-point hike was indicative of “a central bank that wants to stop hiking” as signs of economic pain continue to mount.

Bank of England Signals UK Faces Long Period of Higher Rates

Short-dated gilts gained after the decision on Thursday, but pared much of that move by the end of the day. The two-year yield closed 2 basis points lower at 4.98%. The pound also reversed earlier losses against the dollar and the euro.

A Nationwide Building Society survey this week showed house prices falling at their fastest pace since the global financial crisis for a third straight month, while a gauge of UK manufacturing already stands at recessionary levels.

Even before Thursday, advisers to Chancellor of the Exchequer Jeremy Hunt were fretting that the BOE risks inflicting too much pain on the economy. While the BOE set out weaker quarterly growth projections relative to its last Monetary Policy Report in May, it does not expect a recession.

Jamie Niven, senior fund manager at Candriam, thinks the BOE is nearly done and anticipates lower policy rates than those currently envisaged by markets. He suggests policy makers now favor a “cautious approach,” but were wary of undermining the tightening that’s already been delivered. Their guidance included new language that appears to point to rates remaining elevated for some time, once the tightening cycle is finished.

“It would have been dangerous to communicate this alone given its potential impact on financial conditions,” Niven said. The central bank “therefore prefers to imply higher rates for longer, as opposed to a higher terminal rate followed by cuts,” he said.

Others said it would be hard to imagine the BOE easing up with inflation still so high. Prior to the decision, swaps pricing had implied a one-in-three chance of a larger half-point hike for a second consecutive meeting.

Policy makers are putting “more weight on realised core inflation prints falling rather than what the models say,” said Peter Kinsella, global head of FX strategy at Union Bancaire Privee Ubp SA. “What this means is that the BOE is likely to be in restrictive territory for a lot longer than people think.”

--With assistance from Alice Atkins, Anchalee Worrachate, Naomi Tajitsu, Sujata Rao and Andrew Atkinson.