Risky and safe assets alike have hung on every word and deed of Jerome Powell and Co. for more than a year. Now slowly but surely, the Federal Reserve’s stranglehold over financial markets is easing.

With the latest inflation and labor-market data giving monetary officials fresh ammo to pause their aggressive policy-tightening campaign, attention on Wall Street is shifting to the prospect of an economic downturn. That’s spurring traders to reward the strongest companies in the stock market while punishing the weakest — reducing in-tandem moves between S&P 500 shares.

At the same time, bonds have regained their traditionally negative correlation with equities, rallying amid banking stress and on bets that the era of monetary hawkishness is close to an end. So after reaching a nearly two-decade high in December, a measure of co-movements between assets tracked by Barclays Plc has plunged in recent months.

“Cross-asset correlation remains historically elevated but it’s clearly dropping sharply,” said Barclays strategist Stefano Pascale. “This drop is mostly likely due to bonds reinstating their role as a risk diversifier.”

All that is helping to calm nerves among stock pickers and 60/40 allocators, even as the bond market flashes recession warnings, banking stress builds and a US debt debacle looms.

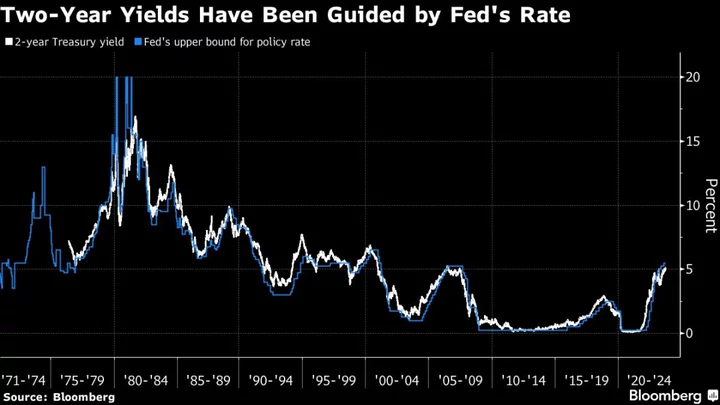

Clearly, the Fed’s policy trajectory on inflation still wields influence over assets. Data on Friday, for example, showed a jump in long-term inflation expectations, sending the S&P 500 slightly lower and yields higher. Still, the central bank’s vice-like grip on investor psychology is getting less extreme while macro-drive market gyrations remain tame. The S&P 500 ended the five days down 0.3%, marking the sixth straight week without a 1% move — the longest stretch of inertia since late 2019.

The reactions are in stark contrast to last year, when the only trading game in town was betting on the Fed’s next hawkish move — causing stocks and bonds to drop in concert. As Chair Powell threatened fresh interest-rate hikes to tame runaway price growth, assets of all stripes trembled on the same monetary headlines. Volatility spiked. And life got harder for money managers as asset correlations spiked — hitting their diversification strategies along the way.

Now though time-honored trading patterns are returning, with bonds serving as a haven asset during times of risk aversion and corporate earnings wielding a strong influence over share movements. What’s more, a semblance of stability has returned. A Morgan Stanley measure that quantifies extreme asset moves has fallen by more than half from the 2022 peak — when monetary turbulence blanketed everything from British government bonds to the Japanese yen.

A Citigroup Inc. study dissecting the underbelly of markets also suggests the influence of macroeconomic forces is subsiding. Using a model that calculates how much the differences among stock returns can be explained by factors like interest rates, Citi strategists including Chris Montagu found macro contribution has fallen to 73% from 80% over the past month — the biggest drop in three years.

At the same time stock traders are gravitating more and more toward companies best positioned to weather an economic slowdown, like tech giants, while dumping shares of the most vulnerable such as energy producers.

The result: Easing lockstep moves among S&P 500 shares. A measure of their three-month correlation dropped below 0.3 in April for the first time in more than a year, according to data compiled by Bloomberg. (A value of 1 means they’re moving in unison with -1 suggesting the opposite.) While it has since risen, the reading remains almost 30% below the average reading last year.

“Since the US regional banking crisis materialized, fear of a recession has moved much higher, and this has generated a lot of repricing at the single-name level as investors focus on companies’ near-term vulnerabilities to a soft economic contraction,” said Peter Chatwell, head of global macro strategies trading at Mizuho International Plc.

Falling equity correlations have been going hand-in-hand with lower gyrations in the broader market. That’s because stock winners offset losers, leading to subdued moves on the index level. The Cboe Volatility Index, a gauge of implied stock swings known as VIX, has been sitting below its one-year average despite economic angst.

Markets and asset classes moving more independently again is good news for active stock managers who tend to benefit when shares move on company-specific factors like earnings and balance sheets rather than macro drivers like monetary policy. Additionally, the reinstated inverse correlation between stocks and bonds is a relief for 60/40 strategies that suffered double-digit losses in 2022 as the two assets dropped in unison on high inflation.

“As we approach peak rates, the focus is shifting to the economic and earnings slowdown — this gives equities a new driver,” said Marija Veitmane, a senior multi-asset strategist at State Street Global Markets. “Furthermore, the ability to defend margins and protect earnings would be a differentiating factor for stock and sector returns.”