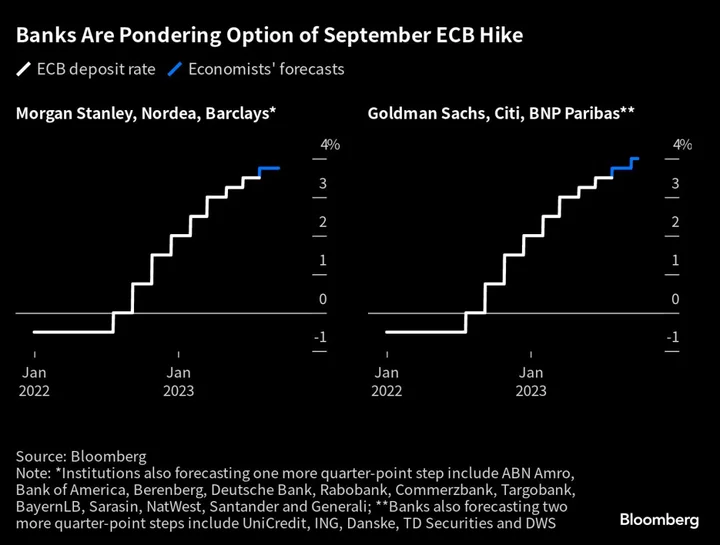

Economists see a greater chance that the European Central Bank will deliver two more interest-rate increases — extending what’s already an historic tightening cycle into September.

Goldman Sachs, UniCredit and BNP Paribas are among banks that have changed their outlook after policymakers delivered a quarter-point hike on Thursday and President Christine Lagarde said there’s more ground to cover to bring inflation back to 2%.

Updated economic projections showed price pressures across the 20-nation eurozone easing more slowly than previously forecast, underpinned by a resilient labor market and strong wage growth.

Most banks though — including Morgan Stanley and Nordea — still see only one more hike in July, highlighting the impact of past increases filtering through to the economy, sluggish growth and likely reluctance among officials to push rates too far.

One More Hike

Morgan Stanley

“When addressing the question on future rate hikes, President Lagarde did not mention September. We read that as a likely reflection of a reluctance within the Council to bring September into the public discussion”

Nordea

“If the ECB is already now prepared to signal another hike for July, it could easily raise rates again in September, unless the updated forecasts show a clearly improved inflation outlook”

ABN Amro

“We are sticking to our view that the ECB will hike only one time further, taking the deposit rate to 3.75%. This is because the ECB is likely to be surprised to the downside on both economic growth and inflation”

Bank of America

“September will likely be a live meeting in line with our view of a terminal of 3.75% with a significant risk of 4% (i.e. a last hike in September). We don’t think current ECB forecasts will survive in September, hence why we don’t change our call”

Berenberg

“If core inflation continues to recede slightly further in coming months, as we expect, and if the data on the real economy are more in line with our call for just 0.3% growth in 2023, the ECB will probably stay put in September after a final move in July”

Barclays

“We make no change to our baseline ECB call of a last 25 basis-point hike in July, bringing the terminal deposit rate to 3.75%. As we indicated in the preview, we think the ECB will keep live the possibility of further hikes after the July meeting and as such the September meeting will remain ‘live’. To this goal, a discussion on a possible pause could be handy at the July meeting. Inflation, activity and credit developments will all enter into the final decision”

Deutsche Bank

“Given the signals, 3.75% now seems a virtually certain outcome in July and sets the minimum level for the terminal rate. As before, we see the risks for the terminal rate as clearly to the upside. 4% in September remains a close call, in our view. It will depend on the data. The Governing Council might not be convinced that a robust slowing in underlying inflation has been proven by the time of the September meeting. We continue to believe that if underlying remains sticky and the Fed is slow to pivot from its tightening bias, the door could even be open to the ECB going above 4% in Q4”

Rabobank

“While the ECB still balances the inflation dynamics, inflation outlook, and the strength of the transmission of its policy, we continue to prefer the more cautious approach of a 3.75% peak and a pause until well into 2024”

Commerzbank

“Another rate hike in mid-September is unlikely. Instead, the ECB is likely to keep the deposit rate at 3.75% for a long time. Unlike the market, we don’t expect interest-rate cuts in 2024, because in the course of 2024 it should become clear that core inflation will not slow further toward 2%”

Targobank

“A rate hike in July remains likely. Only if the economic data in the euro zone continue to be weaker than forecast in the coming weeks would there be a chance for an interest-rate pause. The magic word is: ‘data dependent’”

BayernLB

“Moderating inflation dynamics and sharp transmission of higher interest rates to lending and the real economy (recession) signal that the ECB is likely to end the hiking cycle in September — when new ECB staff projections are released”

Bank J Safra Sarasin

“We continue to expect one last rate hike in July, to a level of 3.75%, followed by at least six months during which rates stay at this elevated level. However, we remain concerned that core inflation rates are not falling sufficiently during this period, such that the risks of our policy rate forecasts are clearly to the upside”

NatWest

“The journey is not over… but it increasingly looks like it will end soon. Lagarde insisted that there was more ground to cover, but the overall tone of the conference suggested that there might not be a whole lot more to do, despite the (limited, after all) upgrade to the inflation forecast”

Santander

“We maintain unchanged our long-held call that the 25 basis-point hike on July 27 could be the last one in this cycle, although the risk is for a longer tightening cycle, a la BoE or Fed, despite the decline in most inflation metrics, given the robustness of the labor market”

Generali

“The ECB growth projections will need to be revised substantially down in September. At the same time, we expect the pass-through of tighter financing conditions to the economy to increase. We continue to expect that the ECB will stop tightening cycle with a peak deposit rate of 3.75% and stay on hold thereafter”

Two More Hikes

Goldman Sachs

“The updated inflation projections point to a higher hurdle to finish the hiking cycle in July” and the ECB’s “communication made no attempt to lay the ground for a pause in the tightening cycle. A higher terminal rate in Europe is also consistent with firmer inflation dynamics in other G10 economies, where we have recently added rate hikes”

Citigroup

“The hawkish forecasts are in our view a clear indication that the ECB is not done yet. From today’s perspective, more than the rate hikes priced in by markets and therefore implied in the forecasts”

UniCredit

“The upwardly revised path for headline and, especially, core inflation into 2025 provides a surprisingly clear indication that the ECB’s tightening job is unlikely to be finished next month. Only a large financial market shock or fast deterioration in the growth outlook could change this, in our view. Therefore, while ECB President Lagarde pre-announced a July hike and said nothing about the September meeting, the balance of risks has clearly titled towards a further rate increase in September, to 4%”

BNP Paribas

“While we continue to think the ECB is too optimistic on growth, and we have a somewhat more benign view on inflation, we do not see enough of a near-term challenge to its new baseline to let it pause already after the July meeting. As a result, 3.75% looks to be a floor for the policy rate, and we expect the ECB to follow July’s hike with another one in September. We continue to expect an extended pause thereafter, with the first cut unlikely to come before mid-2024”

ING

“The ECB will not change its tightening stance until core inflation shows clear signs of a turning point. We won’t be seeing that at the July meeting, and probably not in the September one, either. In fact, we think it would require an economic earthquake for the European Central Bank not to hike in September as well”

Danske

“We continue to expect ECB to hike to 4% by September, and we reiterate our view that the burden of proof will reverse after July when we get two new inflation prints and new staff projections ahead of a September meeting”

TD Securities

“A key feature of the upward revisions to the inflation forecasts came on two fronts. First, the ECB has taken on board past downside errors in its forecasts (i.e., incorporating a view on higher inflation persistence, not unlike the BoE’s recent revisions). Second, President Lagarde pointed to a tighter labor market, leading to higher wages, a feature that has long underlined our expectations of two further rate hikes”

DWS

“While the tighter monetary policy has already led to a decline in lending and a slowdown in economic development, the underlying price trend remains very persistent and poses a risk to the medium-term inflation outlook. Therefore, we do not share market expectations of an end to the tightening path at 3.75% in July. On the contrary, as further high wage increases have already been negotiated and many companies still have enough pricing power, the core inflation rate is likely to remain above 5% until the autumn. We therefore continue to assume that the ECB will have to raise key interest rates to 4% in order to fulfil its mandate in the medium term”