The global economy is shifting toward a higher-for-longer period for interest rates, making the coming flurry of monetary decisions across the developed world pivotal in mapping out that plateau.

In the next week or so, borrowing costs will be set for seven of the world’s 10 most-traded currencies — including the dollar and the euro — with a picture of prolonged policy constriction set to emerge.

There’s suspense on the outcome for some of those decisions, with the European Central Bank’s Thursday meeting too close to call. But there’s a growing consensus that even those set to hold, such as the Federal Reserve, will be keen to reinforce their state of alert about inflation after dropping the ball back in 2021.

Higher-for-longer was the overarching theme that policymakers spoke to at the Fed’s retreat last month in Jackson Hole, Wyoming. And while the onset of the steepest tightening cycle in a generation varied across the Atlantic, a more united sense of purpose is now on show as the prospect of an end to those rate hikes comes into view.

ECB Cliffhanger

First up will be the ECB, whose policymakers face a knife-edge decision on Thursday on whether to keep raising rates or enact a pause.

Economists are almost evenly split on the outcome. Money markets are placing around a 40% chance on a 10th consecutive increase to 4%, down from more than 60% last month, as traders accounted for data pointing to a weakening German economy. A final quarter-point hike hasn’t been ruled out completely, with odds favoring such a move by year-end.

No matter what option President Christine Lagarde and her colleagues go for, an arguably tougher challenge will be to convince financial markets that they will keep policy tight as long as needed to tame prices even as economic growth falters.

She can build on foundations French Governing Council member Francois Villeroy de Galhau started laying as early as January, when he argued that the time that rates remain high matters “at least as much” as the actual level. He now even insists that “the duration matters more.”

Fed Optimism

Next Wednesday, the Fed will take center stage. Officials there are turning more optimistic that they can quash inflation without causing serious economic pain. Bond markets give almost no chance of a rate hike at the upcoming meeting, and economists are in agreement rates will be steady following the clear signals by Fed leaders that they plan to pause any hikes this month.

Amid signs that price pressures and the labor market are gradually cooling, Fed officials don’t want to dash prospects for a “soft landing” by raising rates too much. A Goldilocks outcome would be a rare achievement, and perhaps temper criticism that Fed Chair Jerome Powell reacted too late to rising prices in the first place.

The focus of the Sept. 19-20 meeting will be on updated economic projections that are expected to show another hike by the end of the year, while keeping rates near their peak throughout 2024 to ensure inflation returns to the central bank’s 2% target.

BOE Hawkish

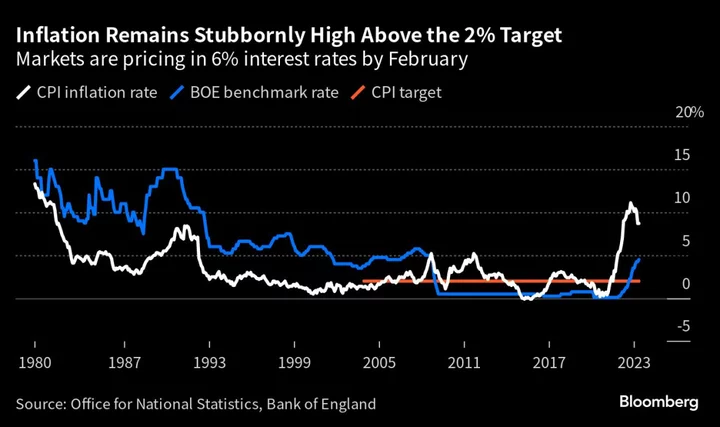

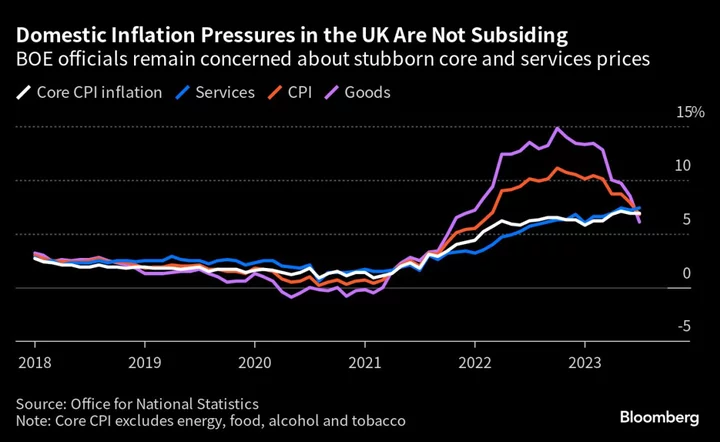

The Bank of England is expected to raise rates a quarter point on Sept 21. After 14 increases running in what’s been the most aggressive tightening cycle in decades, that might be the last, according to economists and market bets. Recent policy guidance suggests it could even be a close vote this month.

In place of concerns about inflation before August, the monetary policy committee is growing increasingly worried about recession. Five of the committee’s nine members have hinted that interest rates at 5.25% are high enough, or almost there.

The message has shifted to lower for longer, with chief economist Huw Pill using South Africa’s flat-topped Table Mountain rather than the sharp peak and descent of Everest as an analogy for the future rate trajectory. Governor Andrew Bailey said last week that rates were “near the top of the cycle.”

Europe

Compared to many of its peers the Swiss National Bank is in a much more comfortable position. With inflation below its 2% ceiling, it may not be forced to raise rates next Thursday.

It’s not clear how much of an appetite officials would have to keep lifting borrowing costs if the ECB calls a pause, given the long shadow across the region that euro-zone policy casts.

The same day as the SNB, Norges Bank in Norway is expected by investors to end rate hikes with a final quarter-point increase in rates. Sweden’s Riksbank, scheduled for then too, may hike borrowing costs again as well.

Japanese Normalization

In Japan, there’s a growing sense that new Governor Kazuo Ueda is paving the way for an eventual normalization of policy.

Ueda told the Yomiuri newspaper in an interview published Saturday that it’s possible the Bank of Japan will have enough information by year-end to judge if wages will continue to rise — a key factor in deciding whether or not to pare back its super-easy policy. That was enough to send the yen higher against all Group-of-10 currencies on Monday.

While that may not lead to a policy change at the Sept. 22 meeting, the last remaining negative rate among major economies appears to be an endangered species.

Canada, Australia

Canada and Australia — both resource-dependent economies — have already had their September decisions and both now appear set for a period of steady rates, even as they signal a willingness to hike again if needed.

Australia’s central bank kept its key interest rate unchanged at 4.1% on Sept. 5 and maintained a tightening bias as Governor Philip Lowe wrapped up his final meeting at the helm with inflation in retreat.

A day later, policymakers led by Governor Tiff Macklem maintained the benchmark rate at 5%, the highest level in 22 years. They acknowledged a downshift in the economy and warned price pressures are proving tough to wrestle all the way back to their target.

Rates Plateau

The argument for a longer-lasting plateau across the world’s major developed economies is that such a policy has similar effects as raising borrowing costs higher and cutting them faster — but with less volatility for businesses and consumers.

But it’s not without risk. If pausing while inflation remains well above targets is misunderstood as central banks going soft, they may be dragged back to the tightening table and have to do even more down the road.

In the euro zone, for example, there’s no denying that expectations aren’t where policymakers would like them. Consumers recently raised their outlook for inflation in three years, and the ECB’s once-favorite market gauge has risen consistently to stand at 2.6%, notably above its 2% goal.

Executive Board member Isabel Schnabel has openly fretted that rising expectations in a slowing economy could be consistent with investors hedging against the risk that central banks aren’t being forceful enough.

In the US, Fed officials have warned they see the possibility of a pickup in economic growth causing inflation to move higher and emphasized the planned September pause should not be seen as a loosening in policy. “Skipping does not imply stopping,” Dallas Fed President Lorie Logan said in a recent speech.

But for now, central banks appear willing to take that gamble, betting a pause that maintains the jobs gains seen through the cycle gives the best prospect for a soft landing.

Atlanta Fed President Raphael Bostic, speaking in Fort Lauderdale last week, said he hopes the US economy can continue to slow down gradually over the next six to 18 months, without a disorderly surge in unemployment.

“If we can avoid that kind of dynamic, that would be a pretty amazing thing,” he said.

--With assistance from Ott Ummelas, Kate Davidson, Zoe Schneeweiss and James Hirai.

Author: Jana Randow, Philip Aldrick and Steve Matthews