Listen to Wall Street’s top economists and you’ll hear the same message again and again: The risk of a recession is fading fast. And yet, in the bond market, the traditional warning that a downturn is near — an inversion of the yield curve — keeps getting louder.

Ed Yardeni, an economist who’s been covering the market since the 1970s, has an explanation.

The yield curve, he posits, is signaling the slowdown in inflation that typically accompanies a recession but not the actual recession itself. He calls this the “Nirvana scenario” — all the gain (an end to nasty price increases for consumers) without much pain (a spike in unemployment or a major hit to the stock market). And that’s manifesting itself in the Treasury market the exact same way that a looming recession would: high yields on short-term debt and lower ones on longer bonds as traders anticipate the Federal Reserve will start cutting interest rates next year.

“It’s conceivable that the interpretation of what the yield curve is saying here is that the Fed managed to succeed in bringing inflation down,” Yardeni, who runs Yardeni Research, said in an interview. “The economy has proven to be remarkably resilient and the Fed may not have to raise rates much higher.”

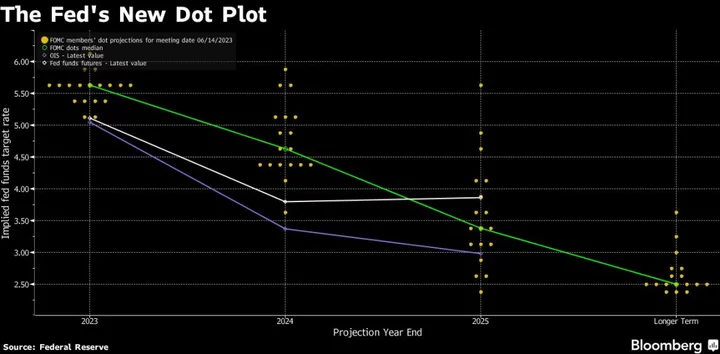

There will almost certainly be at least one more rate increase this year. Traders and economists are in near-unanimous agreement that Fed Chair Jerome Powell will oversee a quarter-point hike when he and his colleagues conclude their two-day meeting on Wednesday. It would be the 11th hike since early last year and bring the benchmark rate to a range of 5.25% to 5.5%.

‘Too Early’

To the camp still committed to the traditional interpretation of an inverted yield curve, the magnitude of this rate-hiking cycle is hard to ignore. At some point, the economic pain will start to mount as banks pare lending to companies and consumers, they figure. Campbell Harvey, the Duke University professor who first established the predictive qualities of an inverted curve back in the 1980s, is perhaps the most outspoken of them.

“It’s too early to say that yield curve inversion is a false signal,” Harvey said in an interview. “The big question is not whether the downturn is coming. It’s how severe it will be. I do worry that the Fed — with two more rate hikes — will put enough gasoline on the fire that is going to push us in a very negative direction.”

So far, the economy has shown surprising resilience. The labor market has remained robust, even if the pace of job growth has slowed, and consumer confidence is strong. Meanwhile, the consumer price index excluding food and energy — which economists view as the best indicator of underlying inflation pressures — rose at an annual clip of 4.8% in June, the smallest increase since 2021.

And the ‘Nirvana’ interpretation of the yield curve is gaining momentum.

Over at At Bank of America Corp., strategist Meghan Swiber is on board: “The curve shape is more a function of expectations for declining inflation than a deterioration in growth.” Economists at Goldman Sachs Group Inc. are urging investors to dismiss the yield-curve’s inversion, saying it’s more reflective of other long-running market trends. And the recent, sharp rally in stocks signals investors have come to the same conclusion.

Banking Crisis

One widely followed slice of the Treasury curve — the difference between 2- and 10-year yields — first inverted in 2022 after the Fed began lifting rates to quell an inflation outbreak. By March, the inversion reached the most-extreme level since the early 1980s as bank failures threatened to crater the economy. Yet even as the banking sector stabilized and those market jitters receded, 10-year yields continued to hold well below those on two-year notes.

What Bloomberg’s Strategists Say...

“The recession suggested by the yield curve inversion will surely still come, and on schedule too. More importantly, there’s no valid reason to even doubt the signal yet. Recession normally comes after the curve has re-steepened into positive territory and we’re a long way from that; we shouldn’t be expecting a recession yet.”

— Mark Cudmore

To read the full note, click here

Over the last two weeks, that gap has widened back to a full percentage point — near the peak levels of the year — even as reports on the economy have largely been stronger than expected. Other segments of the curve are also deeply inverted, including the difference 3-month and 10-year yields, a focus of Harvey’s work.

One reason for the apparent oddity: Overall, rates have risen so high that long-term yields suggest the Fed will wind up easing them slowly back toward more normal levels rather than cutting them dramatically to jump-start growth.

Yardeni said the Fed’s swift moves to instill confidence in regional banks after the collapse of Silicon Valley Bank — through emergency lending that pumped liquidity into the system — may have headed off the type of credit crunch that usually follows an inversion of the curve.

“So far, we haven’t had the economy-wide credit crunch,” he said, “and we haven’t had the recession.”

(Adds Bloomberg strategist comments after 11th paragraph.)

Author: Liz Capo McCormick, Michael Mackenzie and Ye Xie