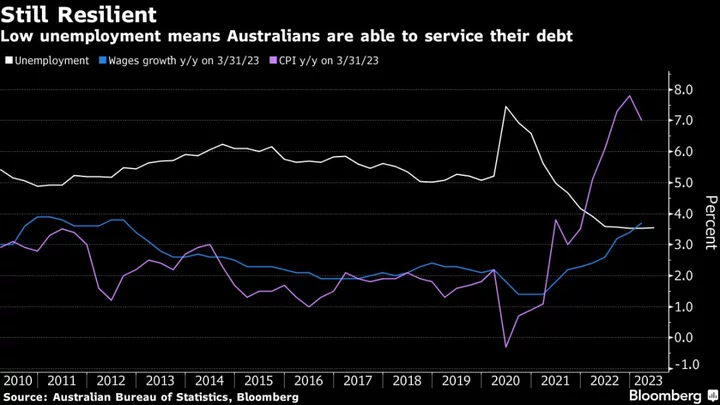

Australia’s home-loan market can easily cope with another 50 basis points of interest-rate hikes without sparking a sharp increase in mortgage arrears, according to S&P Global Ratings.

“Our hypothetical stress scenario shows that most ratings should be able to withstand a moderate level of economic stress,” Erin Kitson, director of structured finance ratings at S&P, said in a webinar on Wednesday, referring to an internal scenario analysis.

The stress test showed Australia’s top-rated Residential Mortgage-Backed Securities will only come under pressure if the Reserve Bank were to lift rates to above 5%, from 4.1% now. RMBS are debt-based assets backed by the interest paid on home loans.

“I think ultimately though, when it comes to mortgage performance, the employment story is key, and that is still largely positive.”

The comments highlight the resilience of Australia’s economy to 4 percentage points of rate hikes in just over a year, with loan arrears still contained and unemployment holding at a very low level of 3.6%. The RBA is seen by economists lifting rates two more times this year to 4.6%.

Kitson expects debt serviceability pressures to rise going forward, especially as a raft of home loans that were fixed at record low borrowing costs come up for renewal in the months ahead.

“In the broader mortgage market a slowdown in refinancing activity, particularly when many fixed rate loans are rolling on to higher variable rates, could lead to large increases in arrears than what we’ve seen currently,” Kitson said. “So far this transition has been well managed.”

Arrears in Australia’s RMBS sector are hovering around a long-term average of 1% at the moment but are likely to climb, Kitson said.

“How much they increase will very much depend on how many more interest rate rises are in the offering, and also how much those interest rate rises start to move the dial on unemployment,” she said.